A Strategic Advisory Guide for Sophisticated Taxpayers and Business Owners

By Jessica Marschall, CPA, ISA AM

President & CEO, MAS LLC | The Green Mission Inc. | Probity Appraisal Group | GM-ESG

December 20th, 2025

As the 2026 filing season approaches, the questions being asked by sophisticated taxpayers are no longer about filing thresholds or basic deductions. Following the enactment of the One Big Beautiful Bill Act “OBBBA” or “OB3” on July 4, 2025, individuals and business owners must now navigate a reshaped tax landscape that combines newly permanent provisions with targeted temporary benefits and intensified IRS enforcement.

This article outlines the most consequential and frequently encountered advanced tax issues facing high-income individuals and closely held businesses—and why proactive planning, rather than reactive compliance, is essential.

I. Advanced Individual Tax Issues

- Net Investment Income Tax (NIIT) Exposure and Planning

Taxpayers continue to underestimate the breadth of the 3.8 percent Net Investment Income Tax under IRC §1411. NIIT exposure often arises unexpectedly from pass-through income, installment sales, rental activity, and deferred compensation. Proper activity grouping, real estate professional status analysis, and entity-level planning can significantly mitigate exposure, but only when executed before year-end.

- True Marginal Value of Itemized Deductions

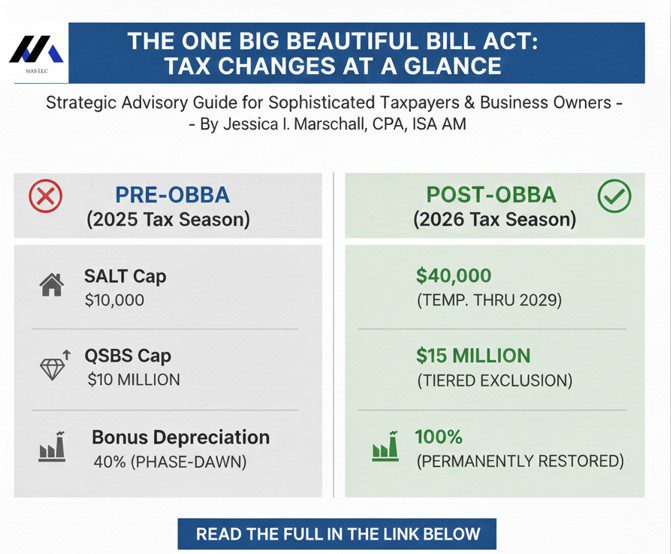

The OBBBA permanently extended the higher standard deduction ($15,750 single/$31,500 joint for 2025), making itemization less common. For those who do itemize, the SALT cap was temporarily raised to $40,000 through 2029 (with phaseouts above $500,000 AGI), reverting to $10,000 in 2030. Advanced planning now focuses on deduction timing, pass-through entity tax elections, and strategic charitable layering rather than simply maximizing Schedule A totals. Additionally, starting in 2026, the benefit of itemized deductions is now capped at 35% for taxpayers in the top bracket (37%). There will also be a .5% of AGI floor for charitable deductions.

- Heightened Scrutiny of Charitable Contributions

The IRS continues to aggressively challenge noncash charitable contributions. Qualified appraisals, contemporaneous written acknowledgments, and strict compliance with Form 8283 are not procedural formalities—they are threshold requirements. Failure results in total disallowance regardless of value or intent. For donations exceeding $5,000, a qualified appraisal must be conducted no earlier than 60 days before the donation date, and the appraiser must sign Part IV of Form 8283, Section B.

- Capital Gains, AMT, and Stacking Effects

Capital gains rarely exist in isolation. The interaction between preferential rates, NIIT, AMT credits, and state taxation can materially alter expected outcomes. The OBBBA made permanent the higher AMT exemption amounts ($88,100 single/$137,000 joint for 2025), significantly reducing AMT exposure for most taxpayers. Gain recognition strategies must account for stacking rules and multi-year income smoothing rather than focusing solely on transaction timing.

- Trust and Estate Distribution Taxation

Trust taxation remains one of the most misunderstood areas of the Code. Distribution planning requires precise DNI calculations, careful attention to state residency rules, and awareness of throwback tax exposure. The OBBBA permanently set the estate and gift tax exemption at $15 million (indexed for inflation), providing long-term planning certainty. Missteps often result in higher aggregate family tax burdens rather than tax minimization.

II. Advanced Pass-Through and Small Business Issues

- Reasonable Compensation in S Corporations

Reasonable compensation audits are increasing in both frequency and sophistication. The IRS has moved its S-Corporation officer compensation project into a specialized team within the Employment Tax Program—a clear signal of continued enforcement focus. For 2025, the Social Security wage base is $174,900. Defensible compensation requires industry benchmarking, role-based analysis, and consistency across payroll, retirement contributions, and profit distributions. Informal “rules of thumb” no longer withstand examination.

- Qualified Business Income Deduction (Section 199A) — Now Permanent

The OBBBA made the 20% QBI deduction permanent, removing sunset uncertainty. The 2025 phase-out thresholds are $197,300 (single) and $394,600 (joint), with Specified Service Trade or Business (SSTB) income fully disqualified above $247,300/$494,600 respectively. The OBBBA also introduced a new minimum deduction of $400 for taxpayers with at least $1,000 of qualifying income, effective 2026. Strategic restructuring, asset segregation, and revenue characterization can preserve deductions, but misclassification creates audit exposure and retroactive adjustments.

- Loss Limitations Under §§461(l), 469, and Basis Rules

Taxpayers frequently discover losses are nondeductible only after filing. The OBBBA made permanent the excess business loss limitation under §461(l), which limits non-corporate taxpayers to approximately $500,000 in business losses annually. Passive activity rules and basis constraints must be modeled holistically. Losses often exist—but timing and deductibility depend on precise structural alignment.

- Owner Transactions and Recharacterization Risk

Unstructured owner draws, undocumented loans, and improperly reimbursed expenses are routinely reclassified as taxable income or constructive dividends. Accountable plans and contemporaneous documentation are no longer optional in audit-resilient planning.

III. Entity Structure and Transaction Planning

- Entity Optimization for Growth and Exit

Entity structures that once worked may no longer align with growth trajectories, investor demands, or exit strategies. Built-in gains exposure, state tax creep, and capital sourcing requirements often necessitate restructuring well before liquidity events occur.

- §351 Transfers and Capital Contributions

Tax-free contributions frequently fail due to debt allocation errors, disguised sale rules, or post-transfer distributions. Basis tracking errors compound over time and surface during exits when correction is most costly. Additional information from our earlier articles are here: The C Corp Conversion Rush: How Section 351 Tax-Free Transfers and Enhanced QSBS Benefits Are Driving Business Entity Transformations

Understanding Section 351: Asset Transfers and Requirements for Tax-Free Treatment

- Equity Compensation and Profits Interests

Equity grants remain a powerful incentive tool but carry valuation, timing, and income characterization risks. §83(b) elections, vesting mechanics, and capital versus ordinary income treatment require careful alignment with both tax and business objectives.

IV. Liquidity Events and Investment Taxation

- Qualified Small Business Stock (QSBS) — Significantly Enhanced

The OBBBA substantially expanded QSBS benefits for stock acquired after July 4, 2025. Key changes include:

Tiered Exclusions: 50% exclusion at 3+ years, 75% at 4+ years, 100% at 5+ years (previously required 5+ years for any exclusion)

Increased Cap: Per-issuer gain exclusion cap raised from $10 million to $15 million (indexed for inflation after 2026)

Higher Asset Threshold: Aggregate gross asset limit increased from $50 million to $75 million (indexed for inflation after 2026)

These changes create significant new planning opportunities for founders and investors, but companies can still unintentionally disqualify themselves. Asset thresholds, redemption activity, and operational tainting must be monitored continuously—not retroactively.

More detail can be found in our article here: Qualified Small Business Stock (QSBS)

- Installment Sales and Earn-Out Structuring

Installment reporting often defers tax but introduces interest imputation, NIIT exposure, and acceleration risk. Earn-outs require careful drafting to avoid ordinary income recharacterization and mismatched reporting.

- Partial Business Sales and Retained Equity

Selling a portion of a business while retaining equity introduces allocation complexity, future tax uncertainty, and valuation disputes. Purchase price allocations drive ordinary versus capital treatment and must be defensible.

V. Depreciation and Cost Recovery — Major Changes

- 100% Bonus Depreciation Permanently Restored

The OBBBA permanently reinstated 100% bonus depreciation for qualified property acquired after January 19, 2025. This reverses the scheduled phase-down (which had reduced the rate to 40% for 2025) and provides long-term certainty for capital investment planning. Property acquired before January 20, 2025, remains subject to the prior phase-down schedule. State conformity varies significantly, requiring state-by-state analysis.

- Expanded Section 179 Limits

The OBBBA more than doubled Section 179 limits. For tax years beginning after 2024, the maximum deduction is now $2,500,000 (up from $1,250,000) with a phase-out threshold of $4,000,000 (up from $3,130,000). Both amounts will continue to be adjusted for inflation. This expansion significantly benefits small and mid-sized businesses investing in equipment and qualified improvement property.

- Cost Segregation Defensibility

Cost segregation remains effective but increasingly scrutinized. Engineering-based studies, proper timing, and documentation quality determine whether accelerated depreciation survives examination.

- New 100% Expensing for Qualified Production Property

The OBBBA introduced Section 168(n), allowing 100% expensing for certain nonresidential real property used in qualified domestic production activities. This includes manufacturing buildings with construction beginning after January 19, 2025, and placed in service before January 1, 2031. This significantly accelerates depreciation on property otherwise depreciable over 39 years.

VI. Multistate and Workforce Complexity

- Economic Nexus Expansion

Wayfair-driven nexus standards extend beyond sales tax. Income tax filing obligations increasingly arise from economic presence alone, particularly for service providers and remote sellers.

- Remote Workforce Tax Exposure

Remote employees create payroll, withholding, unemployment, and apportionment exposure. With 36 states now offering Pass-Through Entity Tax provisions, multi-state operations require careful planning for withholding obligations and state tax apportionment. Many businesses remain noncompliant simply because these issues surface outside traditional accounting workflows.

VII. IRS Enforcement and Risk Management

- Audit-Resilient Documentation Standards

Electronic records, appraisal substantiation, and contemporaneous documentation determine audit outcomes. The IRS is using artificial intelligence and advanced analytics to enhance detection capabilities for tax-compliance issues. The burden of proof increasingly rests with the taxpayer, not the IRS.

- Strategic Use of Amended Returns

Amended returns can mitigate penalties and reduce audit risk when executed strategically. Timing, disclosure scope, and statute considerations determine whether amendment reduces or increases exposure.

- R&D Expense Treatment — Immediate Expensing Restored

The OBBBA permanently reinstated immediate expensing for domestic research and experimental expenditures, reversing the TCJA requirement to capitalize and amortize such costs over five years. Small businesses may elect retroactive application back to 2022 through amended returns. All taxpayers may accelerate deductions for unamortized R&E costs capitalized during 2022-2024.

Final Advisory Perspective

The One Big Beautiful Bill Act has fundamentally reshaped the tax landscape, making permanent many provisions that were previously subject to sunset and introducing significant new benefits. However, this stability should not breed complacency—the increased complexity, new temporary provisions (tips, overtime, auto loan interest deductions through 2028), and intensified IRS enforcement require integrated planning across compliance, valuation, legal structure, and long-term strategy.

These issues represent the true fault lines of modern tax planning. Firms that engage these questions proactively deliver measurable value; those that wait until filing season absorb avoidable risk.

About the Author

Jessica Marschall, CPA, ISA AM, is a tax advisory and valuation professional with 26 years of experience serving as President and CEO of MAS LLC, The Green Mission Inc., Probity Appraisal Group, and GM-ESG. She and her team serve over 400 clients annually in her tax practice and The Green Mission Inc is a national leader in IRS Qualified Deconstruction Appraisals while Probity provides appraisals for other personal property. Jessica teaches CPE courses in advanced tax and appraisal subjects and has authored over 150 articles on tax, valuation, and charitable contribution topics.

Contact: www.MarschallTax.com

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex and subject to change. Consult with qualified tax professionals regarding your specific situation.

© 2025 MAS LLC. All rights reserved.